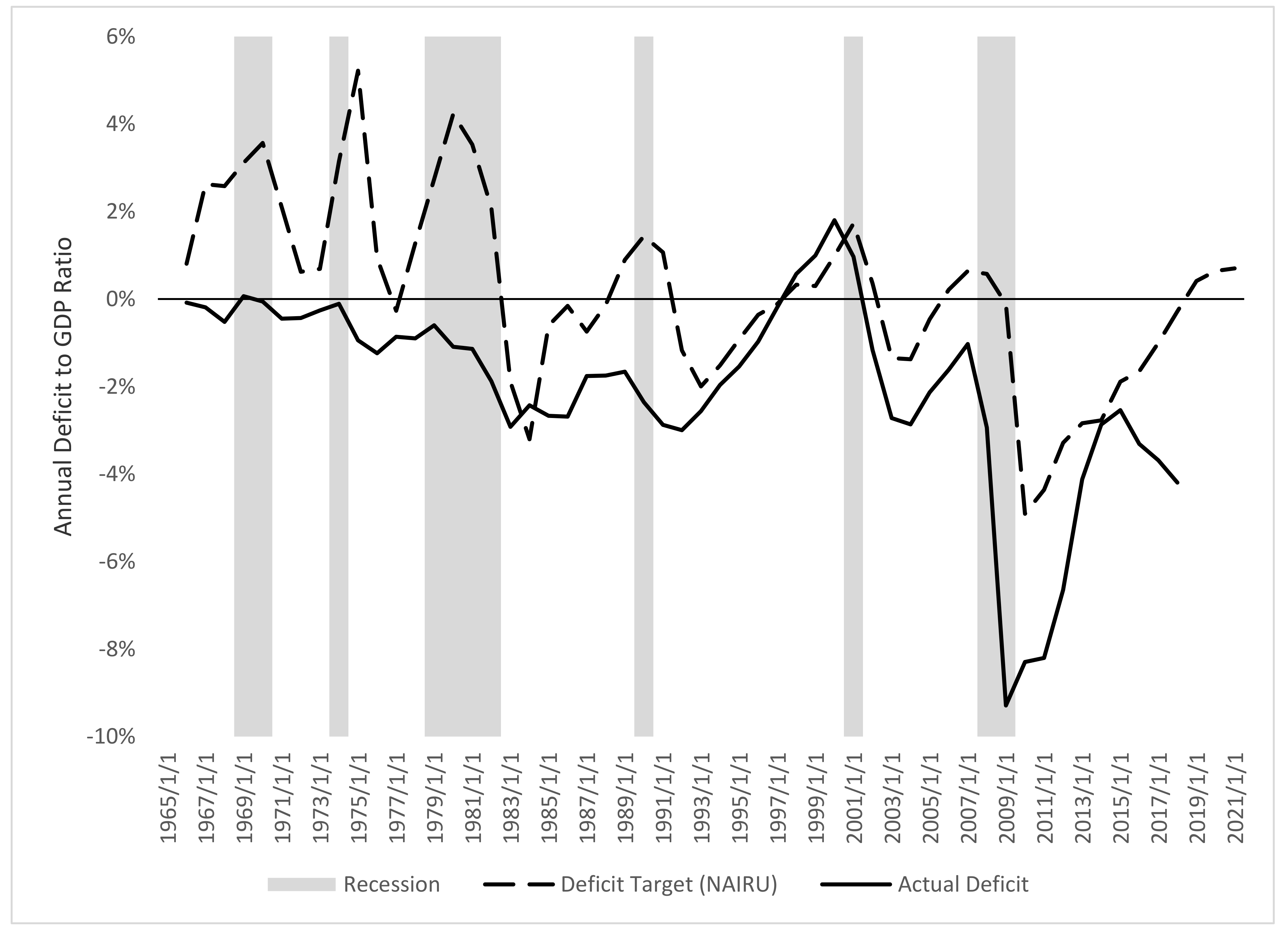

During the a decade from the start off fees, zero organization regarding best 50 having light students’ display of undergraduate enrollment notices parents of their attendees burdened by more two-thirds of the prominent remaining. By contrast, at that exact same era, mothers from attendees at 40-half a dozen of your better 50 institutions to possess Black students’ display out-of undergraduate subscription enjoys about one or two-thirds of one’s principal left, and fourteen universities in which the mediocre brand spanking new dominating try below $ten,000. (Pick Figure A1 in the Appendix step 1.)

The college Scorecard offers investigation into the borrowers’ standard and you may installment standing (borrower-oriented payment pricing). The content just period borrowers’ statuses many years on installment, yet , they highly recommend greatly one Black colored parents happened to be an enthusiastic outsized express of family shedding on delinquency and standard, struggling to pay down their stability.

Sixty-seven associations tell you 10% away from mothers otherwise less making progress once three years; fifty-nine of them was HBCUs. 55

Certainly associations with plenty of analysis about School Scorecard, the fresh new average Parent Also default price 36 months immediately after borrowers go into cost are 7 %, but there is large variation from the college or university. Standard rates can be higher also within many years out of typing repayment, and nowhere is this much more correct than just within HBCUs. At Miles School, Way University, and you may Philander Smith College, inside 2 yrs of your own start of fees more than 20 % from Mother or father Along with borrowers come into standard, exceeding 30 percent by 3rd season. 56 HBCUs make up 30 of your 76 associations where, inside 36 months of your start of the payment, more than 20% off parents default on the Mother Plus mortgage.

Pulled to each other, these types of show greatly advise that Moms and dad Also financing cost try a a whole lot more significant load for Black family compared to light parents in accordance with the mode.

At exactly the same time, the institution Scorecard also provides analysis for the repayment statuses for the majority of subgroups away from children. Such research show that two points gamble key jobs into the parents’ standard rates: perhaps the child finished their program and whether or not the members of the family also acquired this new Pell Offer. At around three-seasons draw, more than twice as many Moms and dad And additionally-borrower mothers off non-completers are located in standard (9.7 per cent) since Parent As well as-debtor parents from completers (a projected 4.8 per cent). 57 At the three-12 months draw, nearly 3 times over doubly certain Mother or father PLUS-debtor moms and dads out of Pell users (a projected nine.3 per cent) got defaulted on their Moms and dad And additionally financing due to the fact Parent As well as-borrower mothers regarding pupils exactly who failed to get the Pell Give (an estimated step three.step three percent). 58

Into the Lifetime from Parent-Borrowers

The content paint an excellent stark study inside the contrasts: together numerous size, Black and you can Latino/a grandfather-borrowers face deeper barriers to help you monetary wellness, which means that deeper traps to help you repayment, than carry out white father or mother-consumers. 61 (On the full gang of abilities, look for Appendix 2.)

For example,920 establishments, the institution Scorecard brings investigation on percentage of Parent Plus consumers progressing on the fund once 36 months, which means that new household was effectively paying the primary count

- Income:62 The fresh average light father or mother just who holds this type of financing brings in far more than $100,000 annually together with the spouse otherwise companion, instead of $fifty,000 so you’re able to $75,000 to own Black mother or father-borrowers and $75,000 to help you $100,000 to have Latino/a daddy-consumers. To thirty-five per cent of one’s Black and you will Latino/a mothers whom keep these finance secure significantly less than $50,000, together with their spouse otherwise companion, that is double the price getting light parents which keep these money (17 percent). (Select Shape 5; remember that such calculations ban domiciles where in fact the respondent was a great retiree.)